Financial stress affects 76% of employees and costs employers an average of $1,900 per worker annually in lost productivity. Companies that ignore this reality face higher turnover rates and increased healthcare expenses.

We at The Pledge believe promoting financial wellness in the workplace isn’t optional anymore-it’s a business necessity that drives both employee satisfaction and bottom-line results.

What Does Financial Wellness Really Cost Your Business

Financial wellness extends far beyond basic budget skills. It encompasses an employee’s ability to manage current financial obligations, prepare for future expenses, and recover from unexpected financial setbacks without compromising their mental health or job performance. The core components include debt management, emergency savings, retirement planning, and insurance coverage. When employees lack these fundamentals, the ripple effects reach every corner of your organization.

The Hidden Productivity Drain

PwC research reveals that 46% of employees consider personal finances their primary source of stress. These workers spend an average of 13 hours per month worrying about money during work hours (according to Mercer data). This translates to three or more hours of daily distraction for over half of financially stressed workers. The math is stark: financially stressed employees are losing 3 hours of productivity each week due to financial stress, costing U.S. businesses significantly.

These workers are twice as likely to seek new employment and take 24% more unplanned absences. The connection between financial anxiety and workplace performance isn’t theoretical-it’s measurable and expensive.

Healthcare Systems Bear the Burden

Financial stress doesn’t just hurt productivity; it drives up healthcare costs significantly. PwC’s 2022 survey found that 34% of employees report financial issues negatively impact their mental health, while 33% experience sleep disruption and 21% see relationship strain. These stress-related health problems create a cascade of medical expenses that employers ultimately absorb through higher insurance premiums and increased healthcare utilization.

John Hancock research quantifies this impact at more than $1,900 per employee annually in combined productivity losses and healthcare costs. This data transforms financial wellness programs from employee benefits into business investments with measurable returns.

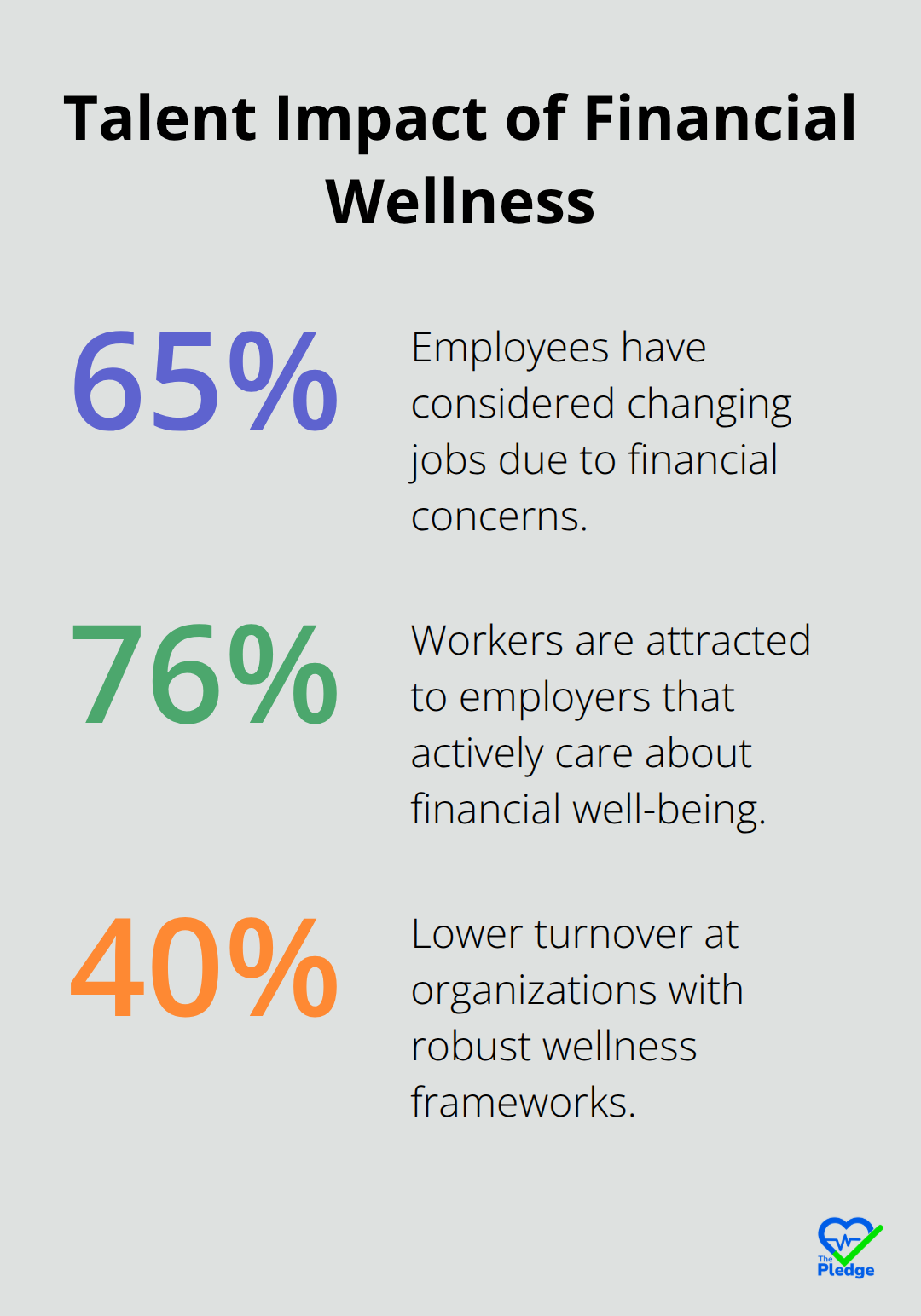

The Competitive Talent Challenge

Companies that fail to address financial wellness face a talent retention crisis. Research shows that 65% of employees have considered changing jobs due to financial concerns, while 76% of workers are attracted to employers that actively care about their financial well-being.

Organizations with robust wellness frameworks experience 40% lower turnover rates and save an average of $3,000 per employee annually in replacement costs. The war for talent has made financial wellness a competitive differentiator that smart organizations can’t afford to ignore.

How Do You Build a Financial Wellness Program That Actually Works

Effective financial wellness programs require three non-negotiable elements: comprehensive educational content, accessible technology delivery, and rigorous measurement systems. Companies that treat financial wellness as a checkbox exercise waste resources and miss opportunities. The most successful programs integrate multiple touchpoints including one-on-one financial counseling, digital budgeting tools, and employer-sponsored savings incentives. With inflation hitting hard in 2023, employee financial stress is on the rise as they navigate higher prices, uneven wage growth and record credit card debt. These challenges provide clear roadmaps for program design.

Technology Platforms Drive Engagement and Results

Modern financial wellness programs succeed or fail based on their technology infrastructure. Employees expect mobile-first experiences with real-time budget tracking, automated savings transfers, and personalized financial goal setting. Companies that use comprehensive platforms see improved engagement compared to traditional educational approaches, as employers increasingly recognize financial wellness benefits as tools to improve worker satisfaction and productivity. The most effective solutions integrate with existing payroll systems to enable automatic contributions to emergency funds and retirement accounts.

Apps that provide spending categorization, bill reminders, and credit score monitoring create daily touchpoints that reinforce positive financial behaviors. Organizations should prioritize platforms that offer both self-service tools and access to certified financial planners for complex situations.

Measurement Separates Winners from Wishful Thinking

Most financial wellness programs fail because employers lack formal measurement systems according to industry research. Successful programs track specific metrics including employee stress reduction surveys, 401k participation rates, and healthcare cost trends. Companies should set specific financial goals before program launch, targeting reductions in healthcare costs within 18 months.

The gold standard involves tracking productivity metrics before and after program implementation-organizations typically see fewer unplanned absences and lower turnover rates. Smart employers also monitor utilization rates across different program components to identify which tools provide the highest return on investment and adjust offerings accordingly.

These measurement frameworks become the foundation for creating sustainable programs that adapt to changing employee needs and economic conditions.

How Do You Create Financial Wellness Programs That Last

Sustainable financial wellness programs demand deliberate culture change rather than surface-level benefits additions. Organizations must normalize financial health conversations through leadership participation and regular communication campaigns. TIAA’s 2022 survey shows that 65% of Gen Z believe companies have responsibility for employee financial wellness, which makes cultural integration essential for program success. Companies achieve permanent impact when executives share their own financial journeys and managers receive training to recognize financial stress symptoms. Regular town halls that feature financial success stories from employees create peer-to-peer learning opportunities that traditional workshops cannot match.

Personalization Drives Engagement Across Demographics

Generic financial advice fails diverse workforces with different income levels, life stages, and cultural backgrounds. Successful programs segment employees into distinct groups: recent graduates who manage student debt, mid-career workers who save for homes, and pre-retirees who maximize 401k contributions. Research indicates that organizations recognize the importance of tailored financial support for improving employee outcomes. Companies should conduct anonymous financial needs assessments to identify specific challenges that face different employee segments. Spanish-speaking workers may need bilingual financial counseling, while hourly employees require different savings strategies than salaried staff (and part-time workers need flexible scheduling for financial education sessions). The most effective programs offer multiple delivery methods that include mobile apps for younger workers and in-person sessions for employees who prefer face-to-face guidance.

Integration With Health Benefits Creates Synergistic Effects

Financial wellness programs achieve maximum impact when they integrate with existing health and retirement benefits rather than operate as standalone initiatives. Health Savings Account education becomes more effective when combined with emergency fund planning, while retirement seminars gain relevance when they address immediate debt concerns. Organizations that bundle financial counseling with Employee Assistance Programs see 40% higher utilization rates according to industry data. Smart integration means companies promote HSA contributions alongside budget planning workshops and connect 401k enrollment with comprehensive financial goal setting. This approach reduces program administration costs while it creates multiple touchpoints that reinforce positive financial behaviors throughout the employee experience.

Technology Platforms Enable Long-Term Success

Modern financial wellness programs succeed when they leverage technology platforms that provide continuous engagement rather than one-time educational events. Employees expect mobile-first experiences with real-time budget tracking, automated savings transfers, and personalized financial goal setting (with push notifications that remind them of upcoming bill payments). Companies that use comprehensive platforms see 60% higher engagement compared to traditional educational approaches. The most effective solutions integrate with existing payroll systems to enable automatic contributions to emergency funds and retirement accounts. Apps that provide spending categorization, bill reminders, and credit score monitoring create daily touchpoints that reinforce positive financial behaviors and build lasting habits. Leadership support determines program success more than budget size or vendor selection.

Final Thoughts

Financial wellness programs deliver measurable returns that extend far beyond employee satisfaction scores. Organizations that implement comprehensive programs see average savings of $3,000 per employee annually through reduced turnover, while healthcare costs drop by 15-20% within 18 months. The 300% ROI becomes evident when companies track productivity gains alongside decreased absenteeism rates.

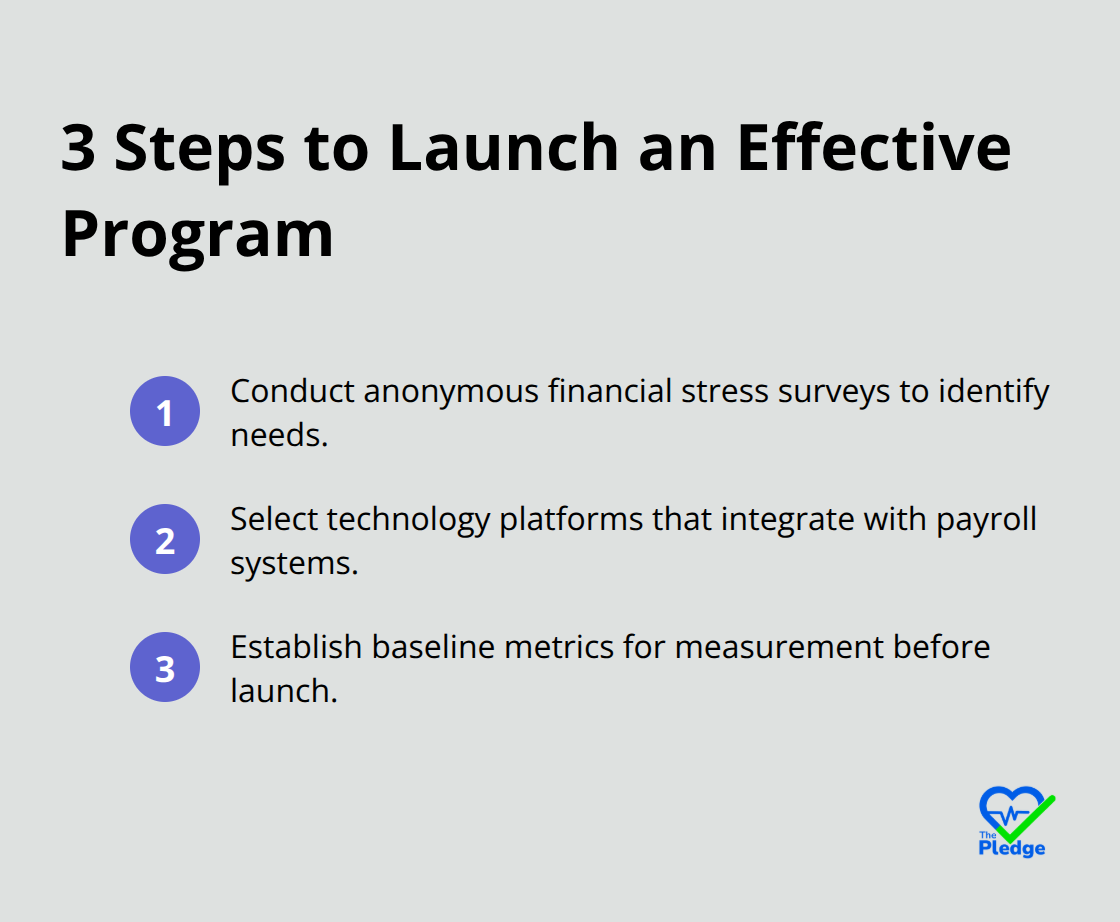

Three fundamental steps launch effective programs: conduct anonymous employee financial stress surveys to identify specific needs, select technology platforms that integrate with existing payroll systems, and establish baseline metrics for measurement. Companies should prioritize mobile-first solutions that provide real-time budget tracking and automated savings features. The future of workplace financial wellness centers on AI-driven personalization and integrated health platforms (with employees expecting financial guidance that connects with their overall well-being programs).

Promoting financial wellness in the workplace has evolved from optional benefit to competitive necessity. Organizations that act now position themselves as employers of choice while building financially resilient workforces that drive long-term business success. The Pledge exemplifies this evolution by centralizing health data and providing personalized wellness programs that achieve superior engagement rates.

![[Guide] Incentives That Drive Preventive Health Participation](https://thepledge.app/wp-content/uploads/emplibot/Guide_-Incentives-That-Drive-Preventive-Health-Participation_1783650286-300x168.jpeg)